I. The Real Cause of the Present Crisis

What is the “deep cause” of the present crisis? It is not the subprime lending, or the housing bubble that might have been reined in. It is not Wall Street greed, or those clever “derivatives” concocted by the financial system or even the reckless borrowing that has characterized almost all sectors of the economy. These factors have all played a role, but they are at best proximate causes.

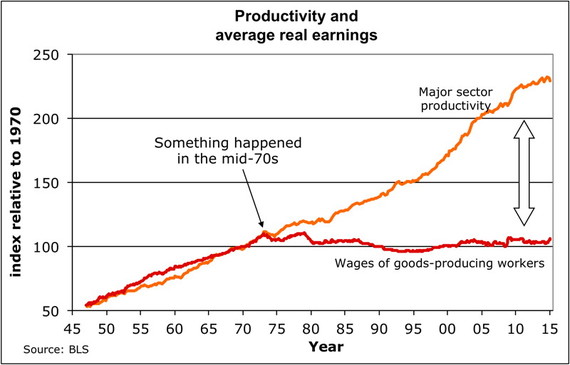

Let me start with a picture:

Productivity vs wages 1945-2015

What we have here is a (simplified) graph showing a steady growth of output per worker in the U.S. economy since WWII, and the corresponding wage trajectory. Wages, you will note, rose in tandem with output until the mid-70s, then went flat. That first period, 1945-75 is sometimes referred to as capitalism’s “Golden Age.” Workers shared in the productivity growth that capitalist innovation produced. But this “social democratic contract” expired in the mid-70s.

At first glance, it would seem that we should have had, for the last three decades, a permanent crisis of overproduction: too many goods relative to purchasing power. With wages held down, who could buy the ever-increasing number of goods being produced?

Certainly, the rich have gotten very much richer during this period of time. But the expenditures of the rich haven’t been nearly enough to keep the economy on track. Ordinary people had to keep buying also, more and more. How? The answer is simple. By borrowing. Credit card debt in the U.S. has increased seven-fold since 1975; home owners took out home equity loans to finance increased consumption; college students went ever deeper into debt to pay for their education, and automobile loans grew and grew. All in all, outstanding household debt in the United States mushroomed from 47% GDP in 1975 to 100% GDP thirty years later.ii In effect, the capitalist class, instead of raising workers’ wages so that they would have the money to buy their goods, were loaning them the money instead.

An analogous scam has been used with the government. Instead of paying the taxes that would cover government spending, the wealthy have loaned the government money—to be repaid with interest, of course.

But this game couldn’t go on. Over-indebted consumers started defaulting. The financial system, which had become an opaque mass of “innovative” new products–mortgaged-back securities, credit default swaps, special investment vehicles, etc. all based on leveraging cheap credit–unraveled.

Okay, we have a crisis. How do we resolve it? Mainstream experts, at least those with any sense, call for a return to Keynesianism. Monetary stimulus: have the Federal Reserve cut interest rates, get money to those banks that are in trouble. Fiscal stimulus: run government deficits, engage in direct job creation. These are moves in the right direction.

But, as we know, Keynesianism has been tried before. With mixed results. We all look back to the Great Depression, and to the New Deal that saved the day. Except it didn’t. It wasn’t President Roosevelt’s job creation programs, noble though they were, that pulled us out of the Great Depression. U.S. unemployment was 3% in 1929. It was still at 17% in 1939, a decade after the stock market crash. As Krugman himself noted in an earlier work, “It took the giant public works project known as World War II–a project that finally silenced the penny pinchers–to bring the Depression to an end.”iii

But there’s not going to be a World War III. Our technologies are too destructive for anyone to seriously contemplate a war among major powers. This is not bad news for us as human beings, but it does close off a path to economic recovery.

If it is true, as I have argued, that ultimately it is too-low wages that are the problem—well, how can Keynesianism fix that? If wages rise, companies will just move abroad. It is that threat that has kept wages flat for so long. We are now living in a globalized capitalist world. Keynesian remedies, designed for relatively self-contained national economies, no longer work.

II. Environmental Crisis

Let me throw another grim consideration into the mix. Suppose I’m wrong. Suppose we do get the global economy growing again, and are able to keep it growing. I don’t think this will happen, but suppose I’m wrong. That will bring us face to face with a crisis of a different sort, a crisis based on the very fact of relentless, limitless growth: the environmental crisis. This one is real in a more profound sense than our current economic crisis, in that it has a material basis, as opposed to a “merely” structural one. We are running down our supply of fossil fuels, depleting our fisheries and forests, pouring too much methane and carbon dioxide into the atmosphere, using too much fresh water, etc., etc.

Of course some will say we can “grow” our way out of this crisis by investing in green technologies, but that’s a fairy tale. Green technologies are important. They help. But it is obvious to all who think seriously about this issue that a long term solution requires shifting our economy to one that does not depend for its health on ever-increasing rich-nation consumption–a consumption that doesn’t make those of us living in rich nations happier anyway.

So we are in a tight corner. Those concerned about rising unemployment urge us to spend, spend, spend, while the environmentalists scream back that our consumption-addiction is killing the planet. And both sides are right. Moreover, both sides really want the same thing: a healthy, stable full-employment economy that treads lightly enough on our fragile planet to be sustainable. This is what we all want, isn’t it?

III. Is Another World Possible?

If we look at world history over the course of the past several centuries, it is hard to miss the fact that democracy has been advancing. The notion that people have the right to rule themselves is an idea of near-universal currency at present, and it shows no signs of weakening.

Democracy has not only extended itself geographically, but in most countries it has deepened internally. Property qualifications have been dropped. Women have been granted the vote. Racial minorities are no longer excluded.

This deepening of democracy has changed the nature of the state. We no longer tolerate a minimalist government that does nothing but maintain our national defenses and enforce law and order. The state is also supposed to provide certain economic services: ensure that our children are educated, our elderly receive pensions, our workplaces are safe, our wages are at least above a bare “minimum,” our air and water are clean, and more.

This extension of democracy into the economic realm is far from complete. Of course further expansion will be resisted. Democratic rights have rarely been granted without a fight. It will always be said that further democratization is unworkable, and, if attempted, will have dire consequences. Such arguments are always made, and yet, to date at least, they (and the powers they represent) have not been able to hold back the democratic tide.

I want to argue that a much fuller economic democracy is on the horizon. It will probably be awhile before we get there–although it should be noted that the rhythms of history are not constant. Long periods of relative structural stability are punctuated by periods of rapid transformation. (Consider the sudden, wholly unexpected, relatively peaceful collapse of the Soviet empire.) In any event, if we know where to look, we can discern, even in the present, economic experiments, political reforms, and intellectual shifts that point to an economic formation vastly more democratic than the one in which we live today, an economic formation that goes beyond capitalism, an economic formation that is—let’s not mince words–a form of socialism.

Is this plausible? Here is Krugman again in a book published three years ago:

Who now can use the words of socialism with a straight face? As a member of the baby boomer generation, I can remember when the idea of revolution, of brave men pushing history forward, had a certain glamour. Now it is a sick joke. . . The truth is that the heart has gone out of the opposition to capitalism.iv

Yet surprisingly Krugman strikes a different note, just a paragraph later:

Capitalism is secure, not only because of its successes–which have been very real–but because no one has a plausible alternative. This situation will not last forever. Surely there will be other ideologies, other dreams, and they will emerge sooner rather than later if the current economic crisis persists and deepens.

IV. Economy Democracy—The Basic Model

There are other dreams, and they are emerging sooner rather than later. Let me sketch for you a picture of one of them, an economic order that could take us beyond capitalism. Let us call it “Economic Democracy,” for it extends democracy into areas essentially off-limits under capitalism. Let me begin, not with an abstract model, but with what we now know in light of the economic experiments of the past century.

We now know that competitive markets are essential to the functioning of a complex, developed economy. This is the negative lesson of the socialist experiments of the twentieth century. Markets cannot be replaced wholesale by planning. It follows that Economic Democracy will be a competitive market economy.

We now know that some sort of democratic regulation of investment flows is essential to rational, stable, sustainable development–for individual countries and for the world economy as a whole. This is the negative lesson of the neoliberal experiments of the last thirty years, now culminating in a global crisis. (Can anyone now say with a straight face that financial markets allocate capital efficiently?)

There is something else we know–at least those of us who pay attention such things. Actually, most people do not know this important fact.

We now know that productive enterprises can be run democratically with little or no loss of efficiency, often with a gain in efficiency, and almost always with considerable gain in employment security. This is the positive lesson of a great many recent experiments in alternative forms of workplace organization.

This fact raises an awkward question. Why is it that in countries (such as mine) that celebrate, indeed almost deify, democracy, that allows us to elect our mayors, our state and local legislators, the national leaders that can send us off to kill or be killed . . . why is it that in such a country we can’t elect our bosses?

The obvious answer is that workplace democracy doesn’t work, that ordinary workers don’t have the competence or self-discipline to select good managers. The problem with this obvious answer is that it is empirically false. There are thousands of successful worker-run enterprises operating around the world. These have been extensively studied. To my knowledge there does not exist a single comparative study that finds the authoritarian (i.e. capitalist) model superior to the democratic one.v

For students of democracy this result is not surprising. To be sure, there are problems with democracy. Excessive debate can be time-consuming, hindering timely action. Good leadership can be stifled if it doesn’t have adequate autonomy. Majorities can oppress minorities. These are standard problems in all democracies, for which there are standard solutions. Representative structures must be put in place; management must be given sufficient autonomy to make difficult decisions without being challenged at every turn; laws must protect minority rights.

With the right structures in place, workplace democracy works. Not perfectly. Bad managers are sometimes appointed. Bad decisions are sometimes made. Democratic firms sometimes fail. But Winston Churchill’s dictum appears to hold: “Democracy is the worst form of government–except for all the others that have been tried from time to time.”

What changes might we envisage that would transform our current capitalism into a democratic economy, one that preserves the efficiency strengths of capitalism, but mitigates its most distressing features? Let’s begin with the basic model. This, of course, is a simplified picture. Any real-life instantiation will be more complicated. But to begin to envisage a viable alternative to capitalism, we need to start with a basic model. This model has three components:

1. A market for goods and services, which is essentially the same as under capitalism.

2. Workplace democracy, which replaces the capitalist institution of wage labor.

3. Democratic control of investment, which replaces capitalist financial markets.

Let me elaborate briefly on each of these key institutions.

1. Historical experience makes it clear that markets (suitably regulated to be sure) are a necessary component of a viable socialism. Central planning does not work for a sophisticated economy. The knowledge and incentive problems are too great. But these markets should be largely confined to goods and services. They should not embrace labor or capital.

2. Enterprises in Economic Democracy are regarded, not as entities to be bought or sold, but as communities. When you are employed by a firm, you have the right to vote for members of a worker council. This council appoints upper management and oversees major enterprise decisions. Although managers are granted a degree of autonomy, they are ultimately answerable to the workforce, one-person, one-vote.

Workers also share in the profits of the enterprise. Workers receive, not a contractual wage, but a share of the profits. These shares need not be equal, but everyone’s income is tied directly to the performance of the firm–hence the incentive to work diligently and efficiently—and to see to it that your co-workers do the same.

3. Some sort of democratic control of investment is essential if an economy is to develop rationally. But control of investment is exceedingly difficult if the investment funds themselves are privately generated. The solution to this problem is simple. Don’t rely on private investors. Generate your investment funds publicly–via taxation. A capital assets tax is the best tax for this purpose—a flat-rate property tax on all businesses. All of these revenues are reinvested in the economy. Each region of the country gets, as a matter of right, its per-capital share. These funds go to public banks, which channel them back into the economy, utilizing both economic and social criteria–including, importantly, employment creation and environmental sensitivity–when making loans.

Would an economy so structured work? The empirical data now available to us strongly support the claim that an economy so structured would work better than capitalism. We know a lot now about regulating a market economy. (We know that laissez-faire doesn’t work.) There is a vast literature now extant on worker-owned or worker-managed enterprises. (We know what problems are likely to arise, and how these can be addressed.) There have been many attempts at macro-economic planning, often involving the allocation of investment resources. We know that intelligent investment planning is possible.

V. Economic Democracy: Two Supplements

The three basic institutions, markets for goods and services, workplace democracy and social control of investment constitute the defining features of Economic Democracy, but there are other structures that should be part of our “new socialism.” Let me just comment on two of them briefly.

1. The government as employer-of- last- resort

It has long been a tenet of socialism that everyone who wants to work should have access to a job. Everyone should have a genuine right-to-work. Long-term involuntary unemployment is not only socially wasteful, but it can be psychologically devastating. Society is saying, in effect, “There is nothing you have to offer that is of any value to us. We may deign to keep you alive, but you are essentially a parasite, consuming without producing.” Is it any wonder that unemployment produces social pathologies?

The solution is simple enough. The government will serve as the employer of last resort. If a person cannot find work elsewhere, the government will provide that person with a job, low-wage, but decent, doing something socially useful.

2. An Entrepreneurial-Capitalist Sector

In my view, Karl Marx’s critique of capitalism remains unsurpassed, but there is an important economic issue that Marx neglected completely, namely the function of the entrepreneur in society. Marx’s analysis of capitalism focuses on the capitalist qua capitalist, i.e. as the provider of capital. This is a passive function, one which can readily be taken over by the state—as is the case in our basic model.

But there is another role played by some capitalists—a creative, entrepreneurial role. This role is assumed by a large number of individuals in a capitalist society, mostly by “petty capitalists,” who set up their own small businesses, but by some “grand capitalists” as well, individuals who turn innovative ideas into major industries and reap a fortune in the process. Clearly, any society that aspires to be technologically innovative and dynamic must provide incentives for this kind of initiative.

Although workplace democracy should be the norm throughout society, it is unreasonable to demand that all businesses conform to this norm. The petty capitalist, after all, works hard. It takes energy, initiative and intelligence to run a small business. These small businesses provide jobs for large numbers of people, and goods and services to even more.

Petty capitalists may provide important services to society, but they do not provide much in the way to technological or organizational innovation. There is also an honorable role to play in a socialist society for entrepreneurial capitalists who operated on a grander scale. Such an entrepreneurial capitalist class need not pose a serious threat to a society in which democratic workplaces are predominant. Democratic firms, when they have equal access to investment capital, need not fear competition from capitalist firms.

Moreover, there are rather simple legal mechanisms that can be put in place to keep this capitalist class in check. The basic problem with capitalists under capitalism is not their active, entrepreneurial role, which, the trumpeting of the ideologists and political candidates to the contrary notwithstanding, relatively few capitalists actually play, but their passive role as suppliers of capital.

Economic Democracy offers a transparent, rational substitute for this latter role—the capital assets tax. So the trick is to develop a mechanism that would prevent the active, entrepreneurial capitalist from become a passive, parasitic one. But such a mechanism is easy enough to imagine: a simple, two-part law stipulating that a) an enterprise developed by an entrepreneurial capitalist can be sold at any time, but only to the state, for a sum equal to the value of the assets upon which the capital-assets tax is paid, and b) the enterprise must be sold when the owner retires or dies. When the state purchases an enterprise, it turns it over to the enterprise’s workers, to be run democratically.

Thus the entrepreneurial capitalists serve two useful, honorable functions. They are a source of both innovation and new democratic enterprises, and thus have a significant role to play in our democratic economy.

VI. Economic Democracy and Economic Crises

I have argued at length elsewhere that Economic Democracy is preferable to capitalism across a wide array of economic and non-economic values. Economic Democracy would not only be efficient and innovative; it would be much more democratic than capitalism, vastly more egalitarian and more rational in its development.vi Nor would it be vulnerable to the kinds of crises just discussed. We would not be vulnerable to the kind of economic crisis we are now experiencing. The basic reason is simple. There are no private financial markets in Economic Democracy. Markets for goods and services remain, but there are no stock markets, bond markets, hedge funds, or private “investment banks” concocting collateralized debt obligations, currency swaps and the myriad other sorts of derivatives that preoccupy investment bankers today. Thus, there is no opportunity for financial speculation.

The financial system is quite transparent. A capital assets tax is collected from businesses, then loaned out to enterprises wanting to expand or to individuals wanting to start new businesses. Loan officers are public officials, whose salaries are tied to loan performances. The loans they make are a matter of public record, as are the performances of those loans. There is nothing mysterious about finance in an Economic Democracy.

Immunity to speculation is not the only strength of Economic Democracy. Even more important, it is not vulnerable to a deep problem we have considered: insufficient effective demand, due ultimately to the fact that wages tend not to keep pace with increases in productivity. For wages are a cost of production in a capitalism firm, and so capitalists strive to keep wages down. But wages are not a cost of production in a democratic firm. Workers receive a specified share of the firm’s profit, not a wage–so all productivity gains are captured by the firm’s workforce.

Capitalism, as we have seen, faces an even deeper problem than the one responsible for the economic crisis now holding us in its grip. Should we succeed in getting our economies growing again (indeed, even if we don’t), we will soon find ourselves an ecological crisis (more precisely, ecological crises–large global ones, many smaller, more regional ones).

Economic Democracy is far better positioned than capitalism to avoid ecological crises. First of all, democratic control over investment means control over development. We can aim for healthy, equitable, sustainable development, not the mindless consumption that fails to make people happy.

Moreover, since funds for investment in an Economic Democracy do not come from private investors, the economy is not hostage to “investor confidence.” We need not worry that an economic slowdown will panic investors, provoking them to pull their money out of the financial markets, triggering a recession. There aren’t any private investors. Economic Democracy can be a healthy, sustainable, “no-growth economy,” whereas capitalism cannot be.

Actually, “no-growth” is a misnomer. Productivity increases under Economic Democracy can be translated into increased leisure instead of ever-increasing consumption. When introducing a more productive technology into their enterprise, workers in a democratic firm have a choice not available to their counterparts in a capitalist firm: they can choose to take those productivity gains in the form of short workweeks, or longer vacations, rather than higher incomes. Given the importance of scaling back excessive consumption, the government can encourage such leisure over consumption choices. It can do so without having to worry about provoking a recession. The economy will continue to experience “growth,” but the growth will be mostly in free time, not consumption.

IX. Conclusion

It is interesting to note that the greatest economist of the twentieth century anticipated such a leisure-based economy. In a remarkable essay written just after the onset of the Great Depression, John Maynard Keynes speculated about the “Economic Possibilities for Our Grandchildren.” He offered a prediction as to what our world would look like a hundred years hence:

We shall use the new-found bounty of nature quite differently than the way he rich use it today, and will map out for ourselves a plan of life quite otherwise than theirs. . . . What work there still remains to be done will be as widely shared as possible–three hour shifts, or a fifteen-hour week. . . . There will also be great changes in our morals. . . . I see us free to return to some of the most sure and certain principles of religion and traditional virtue–that avarice is a vice, that the extraction of usury is a misdemeanor, and the love of money is detestable, that those walk most truly in the paths of virtue and sane wisdom who take least thought for the morrow. . . . We shall honor those who can teach us how to pluck the hour and the day virtuously and well, the delightful people who are capable of taking direct enjoyment in things.vii

Keynes wrote these words in 1930, at a time when “the prevailing world depression, the enormous anomaly of unemployment, the disastrous mistakes we have made, blind us to what is going on under the surface.viii Keynes’s projection was for “a hundred years hence,” i.e. 2030–no longer the distant future. We should ask ourselves: Might there be things “going on under the surface” right now that could bring us to sustainable, democratic, human world? We should ask ourselves, what can we do, now, to hasten the arrival of such a world

I’d like to end on this hopeful note, but there is a poem I read recently that continues to haunt me. It is by Kurt Vonnegut, the author of Slaughterhouse Five–a novel that electrified my generation with its account, based on first-hand experience, of the fire-bombing of Dresden during World War II.. The poem was published shortly before his death in 2007. It’s not a happy poem. It’s entitled “Requiem.”

The crucified planet Earth,

Should it find a voice

And a sense of irony,

Might now well say

Of our abuse of it,

“Forgive them Father,

They know not what they do.”

The irony would be

That we know what

We are doing.

When the last living thing

Has died on account of us,

How poetical it would be

If Earth would say,

In a voice floating up

Perhaps

From the floor

Of the Grand Canyon.

“It is done.”

People did not like it here.

The stakes are very high! A final quote:—one that electrified me when I first read it forty-two years ago, as a first-year graduate student in philosophy:

The philosophers have interpreted the world in various ways. The point, however, is to change it.

–Karl Marx

Endnotes

1 Paul Krugman, “How to End This Depression,” The New York Review of Books (May 24, 2012): 12-14. See also his End This Depression Now! (W.W. Norton, 2012).

2 Barry Cynanon and Stephen Fazzari, “Household Debt in the Consumer Age: Source of Growth, Risk of Collapse,” Capitalism and Society 3, no. 2 (2008): 18.

3 Paul Krugman, “Back to What Obama Must Do,” Rolling Stone (January 14, 2009).

4 Paul Krugman, The Return of Depression Economics and the Crisis of 2008 (New York: Norton, 2009), p. 14.

5 For a sampling of the evidence see my After Capitalism (Lanham, MD: Rowman and Littlefield, 2002), pp. 60-62. See also Gregory Dow, Governing the Firm: Workers’ Control in Theory and Practice (Cambridge: Cambridge University Press, 2003).

6 See After Capitalism, or, for a more technical analysis, Against Capitalism (Cambridge: Cambridge University Press, 1993).

7 John Maynard Keynes, “Economic Possibilities for Our Grandchildren,” In Essays in Persuasion (New York: Norton, 1963), pp. 368-72.

8 Ibid. p. 359.

DEFEND A LIBRARY OF IDEAS

Your $5/month helps preserve a treasure trove of transformative films — free from ads, algorithms, and corporate influence.

Subscribe here.